What are Closing Costs When You Refinance Your home?

04-08-2021About MortgagesEddie KnoellToday we are covering closing costs in relation to refinances. There’s a lot of confusion as to what closing costs are, especially when it comes to getting the prepaids right, and how much they usually cost.

Closing Costs

You can think of your closing costs in the same way you think of a labor charge for getting your oil changed. They’re simply costs that go into every refinance. Closing costs should be simple and transparent, no matter where you go.

Is there ever no such thing as closing costs?

Nope. If someone says there’s no closing costs, they’re trying to pull one on you. Run! That’s not possible.

Is this the same as rolling in closing costs?

Don’t worry about whether or not to roll closing costs in right now. We have another blog post and podcast that digs into all of this. In short, you always have the decision later to roll the costs in or not.

What actually goes into closing costs?

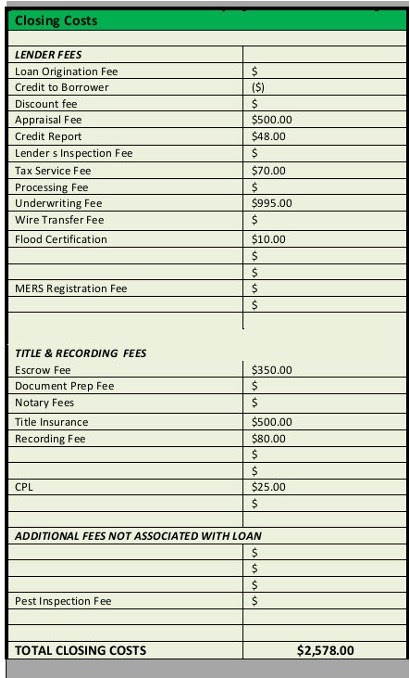

Below is a short chart showing a typical scenario of what you will see with closing costs. In this case, the loan amount is $250,000. From the top you’re going to see an Underwriting fee, or admin/processing fee. Typically, these range from $900 – $1495, but with us it tends to be around $895 or $995.

Next up is a Flood Certification Fee. This is to take a look at the FEMA maps to see if you need flood insurance or not. You should see a fee of about $10 for that. Another fee you’ll see is a Tax Service Fee. The bank is usually going to charge around $70 for that.

We should note that these are not negotiable items.

There’s also the cost of a Credit Report, which is usually around $40 or $50, but we’re seeing them closer to $50 these days. This is because the bureaus are increasing their fees. Right now, we’re seeing usually about $48. It’s often a cost that we incur before the loan actually gets registered. We’re taking a risk, but we’re happy to do it for our clients.

Another fee you’re going to see is an Appraisal Fee. And while there is a chance that we can get you an appraisal waiver, when this is the case, it’s usually due to awesome credit scores and a low loan-to-value. But, in all likelihood, you’re going to need to get that appraisal and it’s going to be around $500. We go through an appraisal management company, so most of our borrowers don’t worry about the appraisals. But even if you do, everything is so regulated and competitive that in most cases things vary maybe twenty-five dollars or so. If things vary more drastically than that there’s a good chance something is missing or something is going on.

You may also see FHA fees at like $550 and VA loans are set at $600 across the country.

Do you pay any of the closing costs upfront?

The only closing cost you should have to pay upfront is the appraisal fee, which is going to be collected at the close. Now you do have the option to roll these in by increasing your loan amount but it’s just the appraisal you should be paying upfront. If you’re not careful the big banks will charge you a non-refundable fee of about $500 bucks. So, be careful before you head to any big retail bank. You shouldn’t be paying any money to the lender in advance.

The title and recording fees

The Escrow Fee here is $350, which is a fairly typical fee. This fee covers the costs of labor that the escrow office does on the file. There’s a lot that goes into that fee: ordering payoffs, collecting, and communicating back and forth with lenders. It’s one of the biggest, thankless jobs that’s a part of the refinancing and purchase process. It’s all done behind the scenes. And when these deals close on time, like ours do, it’s a lot because of what they do for us. We have great escrow officers that work with us, and they’re just awesome. And they make the big difference.

Then, there’s a Title Policy. This covers all the research done to check the chain of title and that you own the property and that no one else has made a claim to it. It’s also called a lender’s title policy and it really is for the lender’s benefit. Now, when you purchase a house, you’re given an owner’s policy, which is a bit different. But when you get a refinance, it’s called the title insurance or lenders policy and they run about $500. This benefits the lender because the lender is going to be giving you hundreds of thousands of dollars, and part of why they’re doing this is because there’s a little insurance policy in place that says, basically, “don’t worry, you’re giving the money to the right person who owns the right home.” You can think of this policy as a kind of insurance that says since the day that you bought your house, no one else has made any claims or anything like that.

The Recording Fee is going to be when the title company records the deed down at the County, and it’s all electronic. Those fees are usually going to range between $60 and $80. Again, this is a raw labor portion of a refinance. Customers can go to whatever title company they want when they do a refinance.

The Consumer Protection Letter (CPL) is required on all purchases and refinances. It’s a small fee, but it’s something that lenders have started charging or asking the title companies for. It’s sort of like a “hold harmless letter,” and the $25 is pretty standard across the industry.

One other thing that you might come across is mobile notary fees due to COVID and offices being closed but once things open back up that won’t be needed anymore.

When all is said and done

In general, about $2500 is a very standard cost for a refinance.

If you have any questions about this or if you have any questions you’d like us to answer on our podcast, you can email your questions to team@azmortgagebrothers.com or give us a call at (602) 535-2171. Be sure to ask us for a free quote on your next mortgage. We’ll personally work with you and help you through the whole process.

•••

Thanks for listening and reading the Mortgage Brothers Show. Let us know if you have any questions you’d like us to answer on this podcast. You can email your questions to Tom@AZMortgageBrothers.com or Eddie@AZMortgageBrothers.com.

Be sure to ask us for a free quote on your next mortgage. We’ll personally work with you and help you through the whole process.

Signature Home Loans LLC does not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only. You should consult your own tax, legal, and accounting advisors before engaging in any transaction. Signature Home Loans NMLS 1007154, NMLS #210917 and 1618695. Equal housing lender.

BACK TO LIST