1% Down Payment - Finally Affordable Down Payment Mortgage Assistance

05-25-2023About MortgagesOwning a home is a dream for many individuals and families. However, one significant hurdle that often stands in the way is the down payment required to secure a mortgage. Traditionally, down payments have been a substantial financial burden, making homeownership seem unattainable for some.

Thankfully, a new solution has emerged to address this issue: the 1% down payment program. Let’s dive into the details of this innovative mortgage assistance program and explore how it has made homeownership more affordable for aspiring buyers.

Understanding Down Payments in Real Estate

Before we delve into the specifics of the 1% down payment program, let's first understand the concept of a down payment in real estate. When a homebuyer pays a down payment, it shows their financial commitment and reduces the risk for the lender.

Traditionally, down payments have typically ranged from 10% to 20% of the home's purchase price, depending on various factors such as loan type, credit score, and lender requirements.

The Challenge of High Down Payments

For many prospective homebuyers, the biggest obstacle to homeownership is accumulating enough funds for a substantial down payment.

The idea of saving tens of thousands of dollars can be daunting, particularly for those already burdened with student loans or other financial obligations. High down payment requirements often result in delayed homeownership or even deter individuals from pursuing their dream altogether.

Introducing the 1% Down Payment Program

The 1% down payment program has emerged as a game-changer in the realm of homeownership. This innovative initiative allows qualified homebuyers to secure a mortgage with just a 1% down payment. Unlike traditional mortgage programs that require a larger upfront investment, the 1% down payment program aims to make homeownership more accessible and attainable for a wider range of individuals.

This new down payment assistance program is a game-changer. With only a 1% down payment required from the buyer, the bank contributes an additional 2% towards the total down payment assistance, resulting in a remarkable 3% down loan. It is important to note that this program entails a conventional loan, not an FHA or VA loan, which adds to its appeal.

Eligibility Criteria and Qualifications

The program has been meticulously designed with a keen focus on affordability, ensuring its high competitiveness in the market. One of its standout features is the fact that it has NO PMI.

This enhances its appeal when compared to a traditional 3% down payment.

Let’s break down the 4 main qualifications for this program:

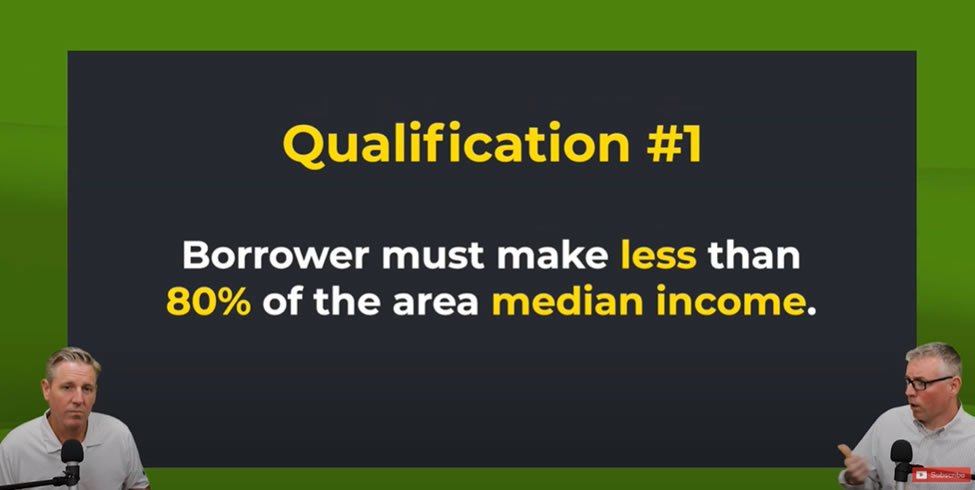

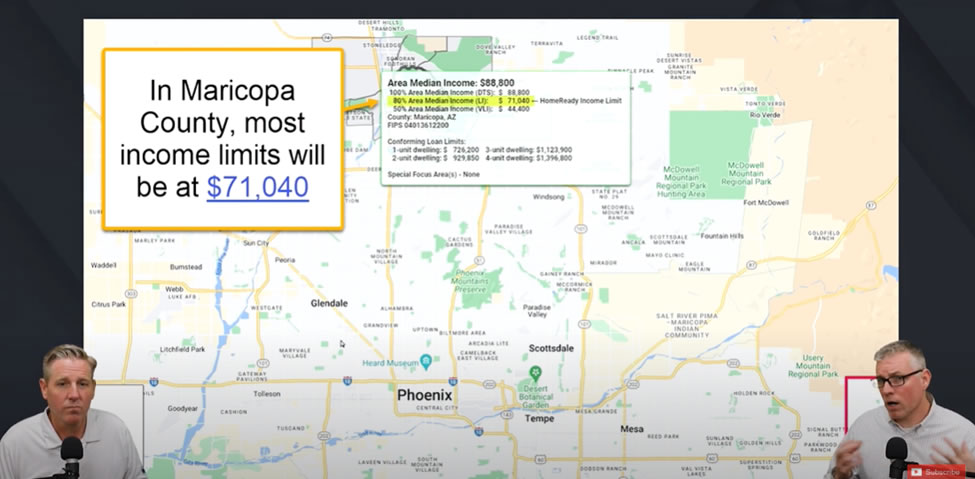

Qualification #1: Income

One of the key qualifications for the 1% down payment program is that the borrower must have an income that is below 80% of the area median income, which in Phoenix and Maricopa County, equates to approximately $71,000. This criterion plays a crucial role in ensuring the program's focus is on assisting individuals who fall within this income range.

This income limit is of utmost importance and emphasizes that applicants must not exceed this income threshold.

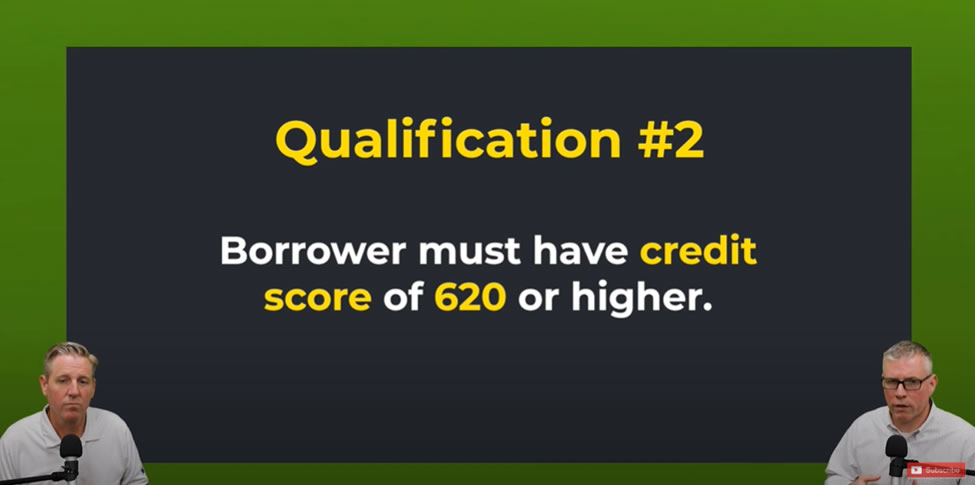

Qualification #2: Credit Score

The second qualification for the 1% down payment program is the requirement of a minimum credit score of 620. While a credit score of 620 or higher is the threshold for eligibility, it is essential to note that the pricing, including interest rates and closing costs, may vary based on individual credit scores.

In cases where the credit score falls within the 620 range, it is worth considering that opting for an FHA loan could be a viable option, albeit potentially affecting pricing factors. However, it's important to stress that 620 is the minimum credit score for eligibility. It is also worth noting that applicants with higher credit scores may enjoy more favorable pricing terms.

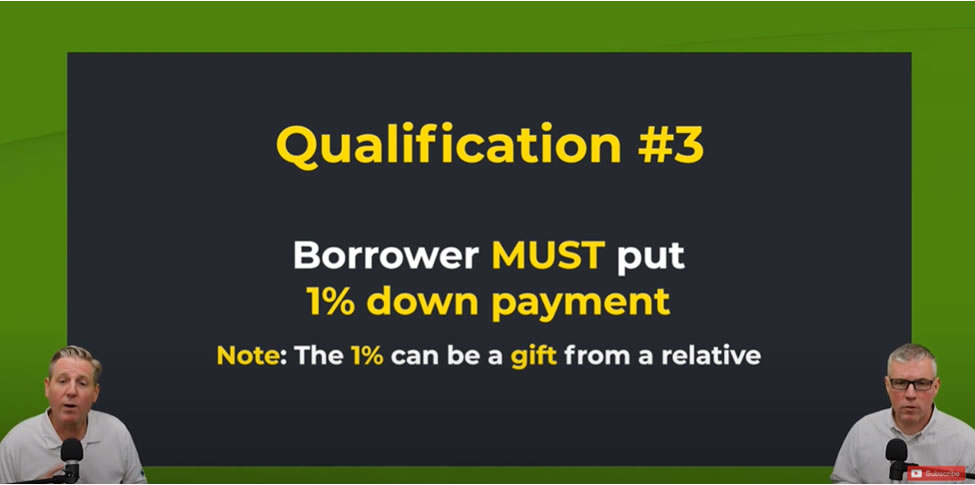

Qualification #3: The 1% Down Payment

The borrower must contribute the 1% down payment. This 1% down payment can be fulfilled through a gift from a family member, which presents a significant opportunity for eligible borrowers. It is essential to emphasize that the gift must originate from a family member, as gifts from friends are not permissible under this program.

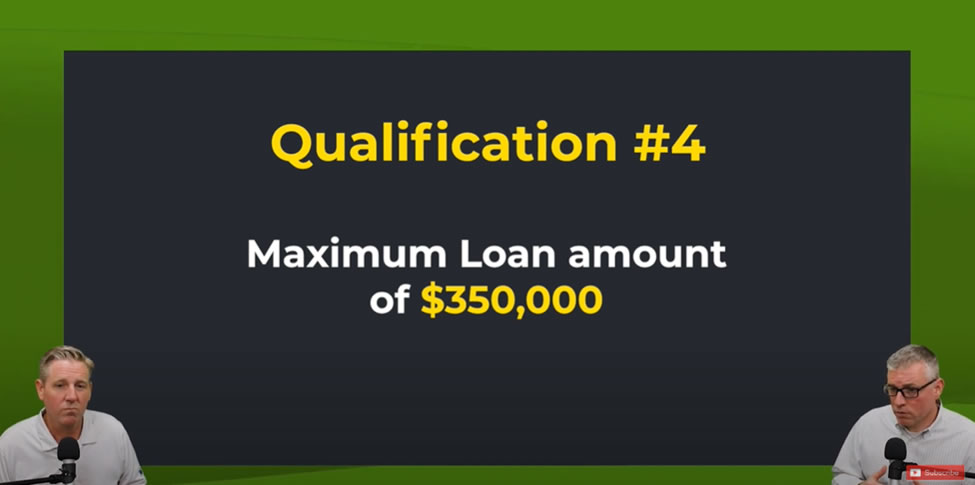

Qualification #4: Maximum Loan Amount

Moving on to qualification number four, it is important to understand that the loan amount cannot exceed $350,000. This limit ensures that the program is geared towards providing support to first-time homebuyers and individuals seeking affordable housing options.

While this program may not accommodate the purchase of homes priced at $500,000, $600,000, or $700,000, it is designed to assist homebuyers in finding suitable homes within the $350,000 range. By focusing on affordability, this program aims to cater to the needs of those seeking a comfortable and reasonably priced home.

How the Program Works

The 1% down payment program operates by partnering with mortgage lenders who are willing to offer this unique financing option. Typically, the program involves a collaboration between the homebuyer and the mortgage lender. The down payment for the loan is 3% (1% from the borrower and 2% comes from the bank).

Benefits of the 1% Down Payment Program

The 1% down payment program offers several benefits to prospective homebuyers. Firstly, it significantly reduces the upfront financial burden, making homeownership more achievable. By requiring only a 1% down payment, individuals can redirect their savings toward other essential expenses or investments. Additionally, the program opens doors for those who may have otherwise been unable to afford a larger down payment, including first-time homebuyers and individuals with moderate incomes.

Potential Drawbacks

While the 1% down payment program provides an opportunity for affordable homeownership, it is crucial to consider potential drawbacks. One potential concern is that a smaller down payment could result in higher monthly mortgage payments.

Also, borrowers must carefully evaluate the terms and conditions of the program, as it may involve additional costs or restrictions compared to traditional mortgages. It is essential to thoroughly understand the implications before committing to the program.

Additionally, borrowers are limited to a loan amount of $350,000 so their purchase price will be limited using this program.

Tips for Saving for a Down Payment

Even with the assistance of programs like the 1% down payment program, saving for a down payment remains a critical step in the homeownership journey. Here are some valuable tips to help you save effectively:

- Create a budget and track your expenses to identify areas where you can cut back and save more.

- Set up automatic transfers from your paycheck to a dedicated down payment savings account.

- Explore homeownership savings programs that offer tax advantages or employer-matching contributions.

- Consider alternative sources of funds, such as a gift from a family member or a withdrawal from a retirement account (if eligible).

- Be patient and stay committed to your savings goal, knowing that each dollar brings you closer to homeownership.

How to Apply for the 1% Down Payment Program

If you're interested in the 1% down payment program, here's a general overview of the application process:

- Check your eligibility by reviewing the qualification criteria provided by the lender. The criteria we outlined above is a general guideline.

- Gather the necessary documents, including proof of income, employment history, and credit information.

- Complete the loan application, ensuring that you provide accurate and up-to-date information.

- Work closely with your lender throughout the process, responding promptly to any requests or inquiries.

- Ready to take advantage of the 1% Down Payment Program? Contact us today to learn more about the application process and get started on your journey toward homeownership with this incredible opportunity.

The Future of Down Payment Assistance

The 1% down payment program is just one example of the ongoing efforts to make homeownership more accessible and affordable. As the real estate landscape continues to evolve, we will likely see more innovative programs and initiatives to ease the financial burden of down payments. These developments hold promise for future homebuyers, providing them with greater opportunities to achieve their homeownership dreams.

Conclusion

We have conducted a quick assessment of the numbers and discovered that the loan amount associated with the 80% of the area median income aligns with what you would typically qualify for. Considering your income at 80% of the area median income, it is reasonable to expect that a $350,000 home would be within your budget. While this loan amount may present some constraints, it remains a realistic figure that we find encouraging. Furthermore, the income requirement of $71,000 per year, coupled with minimal debt, makes qualifying for up to $350,000 attainable.

One aspect we would like to emphasize is the excellent pricing associated with this program. Unlike many down payment assistance programs we have encountered over the past decade, which often entail higher interest rates, this program offers competitive rates that align with standard conventional loans. It is refreshing to encounter a program that provides affordability without compromising on interest rates.

In the past, when borrowers inquired about down payment assistance programs, we often had to caution them about the expenses involved. However, this program breaks that trend by offering a cost-effective solution that surpasses many other options available.

An additional advantage is that the 2% provided through this program does not require repayment if the property is sold or refinanced after six months, which is a significant benefit. Unlike other DPA programs that involve high-interest rates and potential repayment obligations, if you sell or move within five years, you have to pay a portion of that back.

We are genuinely excited about this program and its potential to assist homebuyers. If you have a specific loan scenario or would like to explore further, please don't hesitate to reach out to us via email or phone. As licensed professionals operating in Arizona, we are dedicated to supporting local homebuyers within Maricopa County.

Ready to embark on the journey towards affordable homeownership through the 1% Down Payment Program? Contact us today to learn more about the application process and take the first step toward making your dream of owning a home a reality. Our team is here to guide you through the process and provide the support you need to navigate this incredible opportunity. Don't wait. Reach out to us now, and let's get started.

BACK TO LIST