Reverse Mortgage vs. Selling Your Home

07-11-2022About MortgagesIn this post, we’re talking about reverse mortgages versus selling your home.

It might not be an obvious question to ask, but we’ve been talking with a lot of homeowners who are weighing their options between the two and we figured it was the right time to address this in a podcast and blog post.

We wouldn’t necessarily say that selling your home is an alternative to a reverse mortgage, but a reverse mortgage might be an alternative to selling your home.

What is a reverse mortgage?

A reverse mortgage is a loan that is borrowed against the value of your home. On a reverse mortgage, no loan or mortgage payments are required. Rather, the full balance is due when the borrower either dies, moves out of the property, or sells the home. They’re only available to homeowners who are 62 years old or older.

It can be a great loan for some, but not for everyone. Now, before you make a decision either way we encourage you to speak with a licensed loan officer. This post is just advice, but let’s dig in a bit more.

Who are reverse mortgages for?

Reverse mortgages are a sort of lifestyle loan. If you get one, you’ve likely reached a point in your life where there are certain expenses you need to handle and having the access to the capital is helpful when the alternative is to sell your home and that’s not something you want to do.

Reverse mortgages are for homeowners who want to stay in their homes.

These are for homeowners who love their homes. If there is sentimental value with a long-established deep emotional connection to their home and it gives you comfort and security, a reverse mortgage can give you access to more money without having to worry about moving. If you’re looking for someone else — say your parents — the question to ask would be do they want to leave their home?

Reverse mortgages are for homeowners who are on a limited, or fixed, income.

Reverse mortgages are great for homeowners who are on a limited or fixed income. It can provide a source of money that can be helpful in paying off other expenses that might be difficult to handle otherwise. So, if you’re being squeezed by inflation the cost of living a reverse mortgage might be right for you. This is also where it comes in as an alternative to selling your home. There can be a lot of additional expenses attached to selling your home, so if you aren’t able to afford that and you want to stay in your home, reverse mortgages can be a great option.

It’s also a good option if you can’t afford monthly loan payments or if you can’t qualify for a home equity loan or refinance.

Reverse mortgages are for homeowners who are looking to take out some cash and still not have to make a mortgage payment.

If you haven’t had a payment for years, you need to tap into some equity and you want to take some cash out without worrying about monthly mortgage payments, a reverse mortgage can be a fantastic option.

Who are reverse mortgages not for?

As we’ve mentioned, reverse mortgages are not for everyone.

Reverse mortgages are NOT for homeowners who want to be in their home short term.

Reverse mortgages are not for homeowners who don’t want to be in their home long term. If you’re planning on selling in the next three to five years, we wouldn’t necessarily say a reverse mortgage is ideal for you.

Reverse mortgages are NOT for homeowners who have a dependable monthly cash flow and can afford their quality of life.

If someone has enough cash flow to handle their desired quality of life a reverse mortgage doesn’t really make sense for them.

The cost of a reverse mortgage vs. selling your home

Now, we’re going to take a look at the costs of a reverse mortgage versus selling your home.

What’s the cost of selling your home?

To help you weigh your options, let’s look at an example of the costs associated with selling a home valued at $400,000.

- Sales commissions would be estimated at $24,000 (6% sales commission).

- Seller closing costs from the title company are estimated to be $2,500.

- Moving costs are estimated to be $5000.

In this example, the total estimated cost to sell your home would be $31,500. Then there’s the cost of furnishing a new home, storage costs, or rental costs. And that’s not even all of it. The point is that selling your home isn’t free.

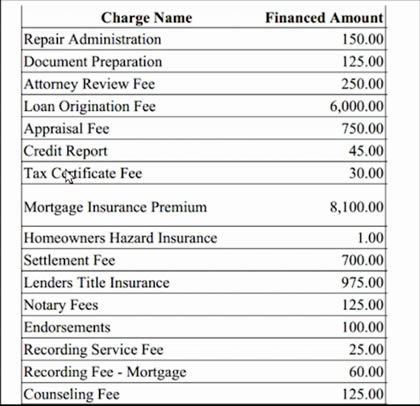

The cost of a reverse mortgage

For a home with the same value of $400,000 and a starting loan amount of $180,000, the total closing costs would be $17,561. Below is a breakdown of a real-life scenario.

The cost of a reverse mortgage and selling your home side to side.

As you can see, there’s a bit of a cost difference between selling your home and getting a reverse mortgage. The ultimate decision of which to choose, however, isn’t one to make in a blog post. If you have any questions about selling your home or reverse mortgages, we’re happy to help. You can send us an email at team@azmortgagebrothers.com or you can give us a call at 602-535-2171.

BACK TO LIST